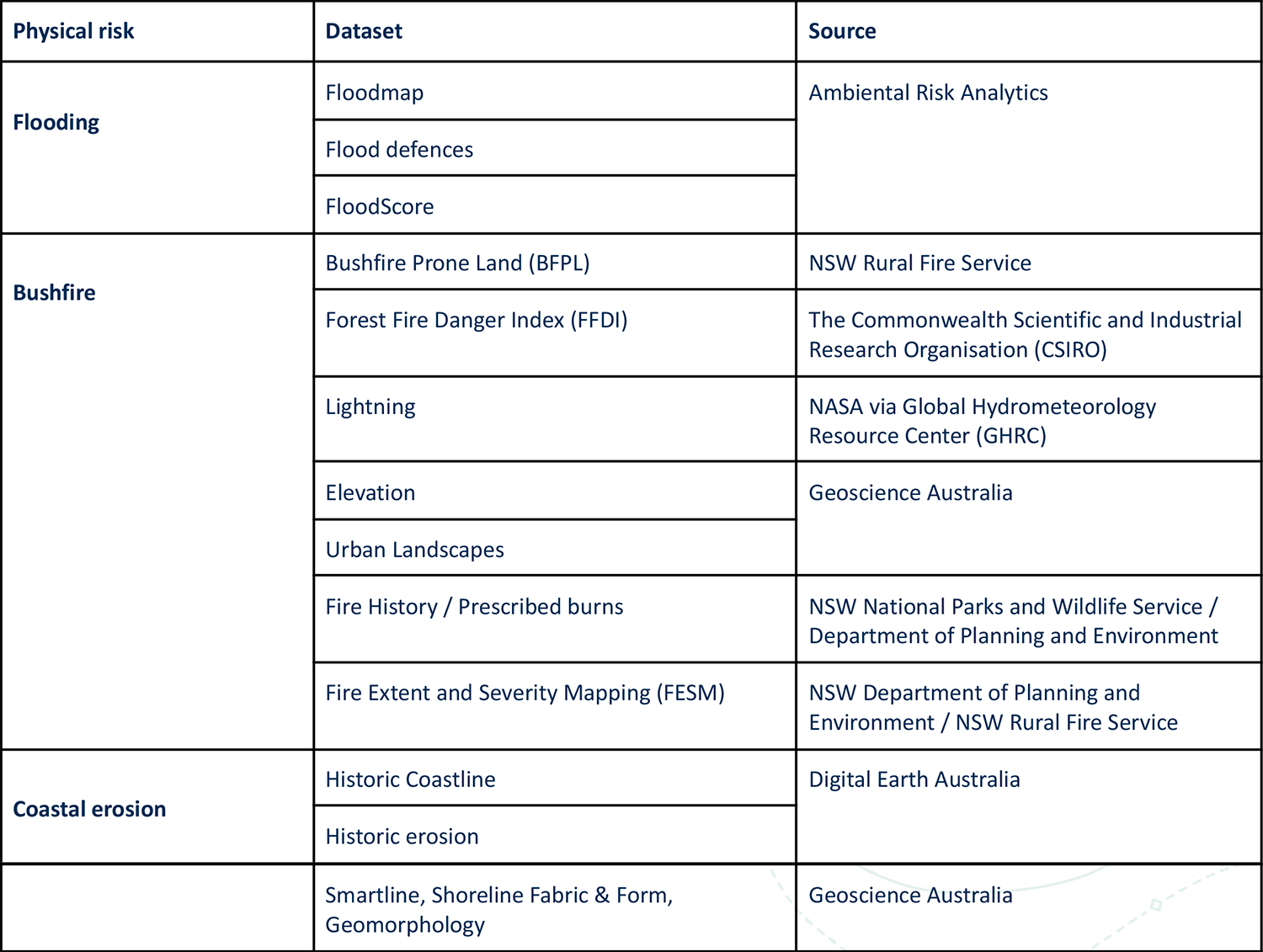

Flooding:

- The undefended flooding data has been sourced from Ambiental Risk Analytics meeting a set criteria specified by Groundsure on likelihood (return periods) and severity (flood depths). The return periods used are 1 in 20, 1 in 100 and 1 in 500 year events in any given year. For example, a 1 in 100 year flood means each year there is a 1 in 100 chance of it happening, not that if a flood occurs, it will not occur again for 99 years.

- Additional data on flood defences has been implemented by Groundsure to mitigate against the presence of flooding where defences are present and data is available, based on likelihood (return period).

- Groundsure has also developed a proprietary calculator to provide an assessment to the whole lot from flooding.

Bushfire:

- Groundsure has developed a proprietary bushfire assessment calculator, utilising a variety of different data inputs not seen in other/existing bushfire risk assessments. This includes:

- Bushfire prone land (BFPL)

- Fire weather from the Forest Fire Danger Index (FFDI)

- Fire history

- Fire extent and Severity Mapping (FESM)

- Urban landscapes and elevation

- To provide the 30 year assessment we have taken the Forest Fire Danger Index data, using decade based long term modelling up to 2096, taking a present day view at 2026 and a 30 year view at 2056.

- Additional datasets including bushfire prone land, historical lightning, historical fires and prescribed burns have been modelled on this same basis.

Coastal Erosion:

- Groundsure has developed a proprietary coastal erosion assessment calculator. This assessment is based on the projected time it will take for the coastline to reach the property. The risk to the property is calculated by analysing multiple risk factors such as:

- Distance to coastline

- Historical erosion activity

- Shoreline fabric

- Shoreline form

- Weather

- To provide the 30 year assessment, historical erosion rates are extrapolated with consideration to the form and fabric of the shore to influence the impact from climate change. The assessment is based on the proximity to the modelled 30 year coastline.

Overall:

- A proprietary overall assessment of risk will be provided in the form of a property specific ClimateIndex™ score (A to F); a summary indication of the risk presented by the included perils (flooding, bushfire and coastal erosion) both today and as impacted by climate change across the next 30 years

ClimateIndex™ is Groundsure’s analysis of climate change risk data. ClimateIndex™ provides a

property specific rating from A to F based on three core physical perils: flooding, bushfire and coastal erosion over 2 time periods: today and 30 years. We have chosen these time frames as 30 years is the assumed length of a mortgage.

ClimateIndex™ has been designed to ensure solicitors are climate compliance ready. It means that there is now a clear, practical and reasonable step which the solicitor can take to discharge their duty of care in respect of such risks.

Solicitors can now advise their clients on future risks which may not only cause physical damage to a property, but also give rise to transition effects, such as having a material impact on the ability to insure or mortgage the property in the medium to long term. In turn, this could affect its future resale value.

When ordering via InfoTrack, an alert will flag when a climate search is required. This will be noted as “critical climate information”.

Norton Rose Fulbright is of the view that many real estate lawyers are obliged to advise on

climate risks and were potentially obliged to do so as early as 2021, when natural disasters first

started being widely attributed to climate change by the media, government and the public.

They consider that specialist climate risk reports would greatly assist lawyers involved in real estate transactions to fulfil their obligations and minimise the risk of claims.

Now that specialist climate risk reports are available as part of the conveyancing transaction, a

lawyer who fails to order such a report (or at least seek instructions to do so), would be at risk of

failing to discharge their duty of care they owe to their client.

In their legal opinion, Norton Rose Fulbright concluded that in many circumstances, a lawyer will

have a duty of care to advise and warn their clients about climate risks.

This duty is based on the tort of negligence and contract, as well as potentially the law of misleading or deceptive conduct, which is a statutory cause of action under the Australian Consumer Law (ACL) including sections 18 and 30 of Schedule 2 of the Competition and Consumer Act 2010.

The duty of care to advise clients on climate risks is especially likely to be the case where one or

more of the following are true:

● It is obvious or well known that climate risks affect the property;

● The lawyer is aware that climate risks may affect their client’s interests;

● The lawyer professes to be a specialist in environmental law;

● The client is vulnerable.

“Providing clients with sound advice to solve a legal problem or dispute requires addressing not

merely the legal issues but also the financial, the emotional and psychological, the relational and

social, the environmental, and the ethical consequences of different courses of action. Clients can

thereby understand the consequences, costs and uncertainties associated with alternative courses of action and make an informed choice. This holistic advice is given by lawyers to clients in many areas of the law on a daily basis. Adding the climate change consequences as a consideration is a natural extension of this everyday practice.” [emphasis added] Chief Judge Brian Preston of the NSW Land

and Environment Court.

Failure by lawyers to follow reasonable steps to discharge their duty may increase their exposure to liability risks, including clients seeking damages for professional negligence, increased professional indemnity insurance premiums, and possible reputational damage.

As reports and tools are now available which analyse the risks climate change presents to property, lawyers will now be in a position to provide more meaningful and timely advice to their clients, and should pass such reports or tools onto their client. However, the extent to which a lawyer is required to go further and provide advice on the implications of the report has two opposing views:

- Lawyers should not be compelled to provide opinions which they are not qualified to give, including in relation to the financial wisdom of a transaction; and

- It is incumbent on a lawyer to advise their client of the obvious practical implications of the client’s entry into the transaction that is the subject of advice.

The courts generally reconcile these two considerations by allowing lawyers to discharge their duty of care by bringing the potential issue to the clients attention and simply recommending they seek further advice from a specialist lawyer and/or other expert, such as Groundsure. See Hatzitanos & Ors v Jordan.

As per the above, if a lawyer is able to obtain a report which assess how climate change is likely to impact a property, it may not be necessary to summarise the findings of the report, particularly if it:

- Is already in a digestible format and written in plain English; and

- Discusses how climate change may impact the value, insurability and availability of finance and development potential of the property, and the kinds of further advice which it may be useful to obtain in relation to those impacts.

Where a report indicates a relatively high risk, it may be necessary for the lawyer to recommend, in strong terms, that their client seek further advice.

Failure by lawyers to follow reasonable steps to discharge their duty may increase their exposure to liability risks, including clients seeking damages for professional negligence, increased professional indemnity insurance premiums, and possible reputational damage.